Money.co.uk’s cost of living statistics revealed that at a retirement age of 65+, an average pension of £19,000 is needed to live alone in the UK. But with spending tightening across the country, are employees in certain industries facing greater cuts to their pension contributions than others?

The savings experts at money.co.uk looked at the most recent Office for National Statistics pensions contribution figures to reveal how pension contributions have changed in each industry across the UK over the past years. And from this, the estimated future trends in the next five years.

Employer pension contributions over the last five years

Only three out of 16 industries saw an increase in employer pension contributions at the end of a five-year period from 2017 to the latest ONS figures from 2021.

Public Administration, along with the Education sector, had the highest employer pension contributions at 15-20% in 2017. While Education industry contributions remain the same, Public Administration contributions have risen to above 20%, the highest among all industries analysed.

Financial and insurance sector employer pension contributions increased from 8-10% to 10-12% between 2017 to 2021 and remain at the same level now. For the real estate industry and transportation industry, it fluctuated over time but currently stays in the same 8-10% bracket.

The administration sector had the lowest employer pension contribution, at less than 4% in 2017 and 2018. This increased to 8-10% in 2019 and remains steady.

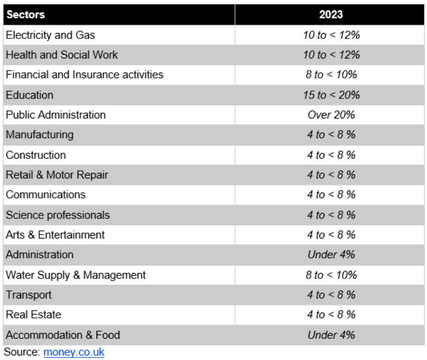

Table 1: UK pension contributions by industry in 2023

Public administration is the only sector with an expected increase in employer contributions over the next five years

Currently, the public administration industry has the highest employer pension contributions at 20% and above, followed by education at 15-20%. Behind are health and social work and electricity and gas at 10-12%. Out of these industries, education is the only one that will see an increase in pension contributions, rising from the already above-average 15-20% to more than 20% by 2028.

Five industries are set to see a reduction in pension contributions this 2023

Money.co.uk predicts that six out of 16 industries will see a decrease in employer pension contributions in the next five years, with five industries already experiencing a decrease in 2023. Only retail and motor repair will have more time to prepare for a reduction in pension contributions, which is predicted to happen in 2026, while employees in the construction industry can anticipate it as early as 2023.

Financial and insurance activities currently receive a pension contribution of 10-12% but will see their retirement funds reduce to 8-10% already this year, a number that it’s likely to remain the same until 2028.

Transportation, real estate, and water supply and management have their retirement funds at a bracket of 8-10%. The transportation and real estate sectors are predicted to have it reduced to a bracket of 4-10% already in 2023 until the next five years.

At a current range of 4-8%, the construction, retail and motor repair, and administration industries are expected to fall to below 4% and revert close to the 3% minimum in pension contributions by 2028. Additionally, retirement funds for the accommodation and food service industry is also expected to remain at less than 4% by 2028. The sector has not seen an increase in employer pension contributions since 2014.

Lucinda O’Brien, personal finance expert at money.co.uk, provides guidance on saving for retirement:

“With inflation at an all-time high in 40 years it has created a fluctuating economic environment, so that both employees and employers are impacted. If savings are not made outside of pension contributions, it can negatively affect retirement savings further down the line.

- “Budget weekly, monthly, and yearly – To properly plan for your financial health, saving for your future must be taken into account alongside immediate short-term spending. Create a budget plan for each week, month, and year to ensure that you are correctly planning for your future. Aim to meet saving targets for each year to ensure that you are contributing to your pensions in your personal savings too.

- “Build an investment portfolio – Diversifying your savings is a great way to generate returns on it that are greater than what is offered by your bank’s savings interest rate. However, always do your research as investing carries some risk.

- “Utilise a Lifetime ISA – Best used for buying a property or saving for later life, those who are between the ages of 18 and 40 should open a LISA account. It allows you to save up to £4,000 each year with the government contributing an additional 25% to your savings (£1,000 max).

- “Transfer your debt to pay less interest – If you are carrying credit card debt that you know you cannot pay off with one payment, consider balance transfer credit cards. This allows you to debt from one card (or several cards) to another card from a different provider. The aim is to switch to a credit card that offers a lower interest rate or no interest for a set time which will allow you to make repayments without accruing more debt in the meantime.

- “Set a savings goal” – Setting a savings goal begins with working out how much spare income you can put towards your target each month. For short term goals like holidays or home appliances, a savings pot within your bank would be the best way to set aside money. For long term goals like your retirement fund or deposit for a house, a lifetime ISA allows you to save up to £4,000 a year tax free with a government contribution.”

Money.co.uk best savings account